Understanding Cost of Capital – Finance

Equity Capital

When a company raises capital through the issue of ordinary shares it is effectively borrowing from the capital markets on a permanent basis. There is no maturity date associated with the shares and hence the loan is never repaid. Since the company is permanently in debt to the ordinary shareholders, the latter are the ultimate owners of the enterprise – a relationship recognized in law. The implication is that the enterprise’s business activities ought to be guided by the shareholders’ interest in wealth maximization. In other words, it should seek to maximise the rate of return on equity.

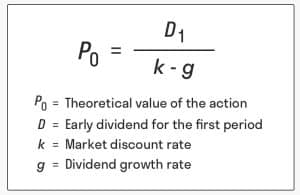

From the perspective of the enterprise, the return on equity is a cost associated with acquiring use of the shareholders’ capital. Indeed, if we assume that the enterprise is financed solely by equity then its aggregate cost of capital is equal to the shareholders’ required return on equity. The impact of the cost of capital on shareholders’ wealth is expressed in the Dividend Valuation Model (DVM):

Where: P0 = Current share price

d0 = Latest dividend payment

d1 = Next dividend payment

g = Dividend growth rate

k = Cost of equity capital

The DVM states that the current share price (the fundamental measure of shareholder wealth) is a function of the latest dividend payment, the dividend growth rate and the cost of equity capital. It should be obvious that the higher the cost of equity the lower the share price3.. How is the cost of equity determined? In formal terms, we just need to restate the DVM in terms of the cost of equity:

This approach to estimating the cost of equity capital states that it is a product of three components, the latest dividend payment, the dividend growth rate and the current share price. As a solution it has certain strengths, not least the fact that the determinate values are easily obtainable, thereby making the calculation a straightforward exercise. More importantly, it is consistent with the argument that the objective of the firm ought to be the maximisation of shareholder wealth. However, it is still a somewhat formal solution to k:, it simply reworks the problem of determining a company’s cost of equity into one of determining its dividend growth rate (g).

There is a significant amount of uncertainty concerning dividend payments from one period to the next. Unexpected changes in future profitability, in future levels of reinvested profits and in management-controlled dividend policies mean that future dividends cannot be known with certainty. Hence, the dividend growth rate is, at best, an estimate. A common approach to estimating g involves simply extrapolating the historical dividend growth rate into the future. This can be adjusted by quantifying the effects of any additional factors that might be expected to produce a change in future growth rates. A second approach, suggested in the work of Myron Gordon, specifies g in terms of two factors – the proportion of total earnings retained for reinvestment (b), and the return on capital employed (r), i.e.:

The logic behind this equation is that for a company to raise dividend payments over time, it must generate greater profits by increasing its investments in fixed assets. The greater the proportion of current profits retained for reinvestment at the rate of return r, the higher the dividend growth rate. In other words, high rates of reinvestment of current earnings will generate a more rapid rate of increase in future earnings and, hence, facilitate higher dividend growth rates

One limitation of Gordon’s model of dividend growth is that it is only applicable to all-equity financed companies. Once debt is introduced into a company’s capital structure the equation no longer of necessity holds. Growth in earnings and, therefore, dividends can now be generated independently of retained earnings.

The Cost of Debt Capital

When discussing debt capital in its generic form, standard textbooks in financial economics utilise the example of marketable bonds paying a regular, fixed amount of interest over a specified period of time as the representative form. As mentioned earlier, debt capital appears in many different guises. Nevertheless, there are good reasons why the ‘straight’ bond is portrayed as the archetypal form of debt capital. It provides the most convenient form for specifying an economic definition of the yield on a particular debt instrument, and the relationship between yield and market value. A simple scenario should help clarify this. The interest payments on bonds are quoted as a fixed percentage of its par value (normally set at £100 in the UK), meaning that the interest payment is fixed in cash terms. However, it is likely to be a misleading indicator of the economic return from an investment in bond. If a bond happens to be trading at £100 in the market, then the ‘coupon’ rate and economic yield are the same. But what if the bond can be bought for less than £100? The investor still receives the same cash flows (in the form of interest payments and the redemption payment) but has undertaken a smaller outlay. This implies that the yield (more formally, yield to maturity) is higher than the coupon rate. Likewise, if a bond costs more than £100 (it is trading at a premium to its par value) it implies that the yield is below the coupon rate. In effect, the yield to maturity is a truer measure of the rate at which monetary wealth accumulates over the period of the investment than the coupon rate.

The yield on an investment in debt securities can, initially at least, be regarded as the mirror image of the cost that the issuer of the bonds is paying for use of the debt capital. In other words, it can also be seen as a measure of the cost of debt. This should not be too difficult to grasp. After all, if investors are receiving a yield of x per cent, then it is not unreasonable to state that the company must therefore be paying x per cent. However, there are two qualifications that need to be made to this statement.

Firstly, assuming fixed coupon rates, the cost of the capital raised by the company is established at the point when the bond issue is undertaken. What happens to yields and bond prices over the subsequent life of the debt does not alter the terms on which the company originally borrowed the funds. However, subsequent developments will affect the terms upon which further funds can be borrowed. In other words, changes in yields are an important consideration for the company because it implies that the cost of any new debt is subject to change. The example of callable bonds helps to clarify this point. The main reason why a company might wish to sell bonds with a call facility attached is that it believes that yields (and therefore, the cost of capital) are liable to fall in the future. If yields do fall, then the company will be able to call in its existing ‘high yield’ bonds, using new funds borrowed at a lower rate to meet the redemption payments. In net terms, the company has the same level of debt but is paying less interest (It should be pointed out that investors would require a higher return on callable bonds compared to non-callable bonds of the same class. In other words, the advantages to the company associated with the call option cannot be procured free of charge).

The second reason why it is somewhat simplistic to equate the yield on bonds and the cost of debt is that interest on debt is tax deductible. Interest payments are deducted from profit before tax. Hence, using debt capital reduces the amount of tax payable. The upshot is that it is more correct to talk of the after-tax cost of debt capital.

Debt versus Equity

For the individual company, debt capital should be cheaper than equity capital. Shareholders, after all, take on more risk than creditors and will expect the scale of rewards to reflect this. Debt capital also generates tax benefits that further reduce its cost. In fact, the differential tax treatment of interest on debt compared to dividends on shares has been a central issue in academic deliberations over the financing decision. This point will become clearer later in the unit when we examine the arguments of Franco Modigliani and Merton Miller regarding the financing decision.

Warrants and Convertibles

Companies sometimes raise debt capital by issuing securities that provide investors with an opportunity to acquire equity. There are two types of instruments that facilitate this – equity warrants and convertibles.

An equity warrant is an option contract that entitles the holder to purchase a pre-determined number of shares in the company at a fixed price. They are issued as attachments to bonds and can be exercised at any time during their life. The appeal of warrants is that they allow investors to gain from any rise in the share price while being protected against downside movements. If the company’s share price rises sufficiently, investors can exercise warrants and thereby obtain shares at a cost below the prevailing market price. On the other hand, if the share price falls warrants will not be exercised. Hence holders of warrants do not lose to the same extent as the existing shareholders.

For the company, the appeal of warrants is that they make the underlying debt instrument easier to sell and thereby allow debt capital to be raised at a lower cost. However, the company has to bear in mind that the exercise of warrants increases the amount of equity capital. Existing shareholders may resent the consequent dilution of ownership that might arise from the exercise of warrants on as large scale. In addition, while warrants may help reduce the cost of debt, the equity raised through exercise will be expensive. Warrants are likely to be exercised when the market price of the company’s shares has risen substantially above the warrant exercise price. In effect, the company is forced to sell new shares at a price below what it might otherwise have been able to command, thereby making the capital expensive.

Convertibles are bonds that can be converted into ordinary shares at some future date. A conversion ratio is stated, indicating the number of shares that can be acquired for the bond. Unlike a warrant, the exercise of a convertible does not result in any additional capital being raised. It merely produces a replacement of debt capital with equity capital. They are designed to appeal to investors in ways similar to warrants. In other words, they provide an opportunity to profit from increasing share prices without being exposed to the danger of share prices falling. However, the upside potential may be limited by the fact that most convertible bonds are callable by the company. If the share price rises to a level where the value of the shares from conversion is equal to the call price offered for the bond by the company then there is an incentive for the company to call in the bonds. In effect, the call price puts an upper limit on the value of a convertible bond.

For more details you can visit our website at https://www.helpwithassignment.com/finance-assignment-help

Book Your Assignment

Recent Posts

How To Prepare An Excellent Thesis Defense?

Read More

How to Restate A Thesis? – A Detailed Guide

Read More

Explanatory Thesis: Examples and Guide for Clear Writing

Read More

How To Write 3 Types Of Thesis Statements?

Read More

How to Effectively Prepare for Your Thesis Defense?

Read MoreGet assignment help from subject matter experts!

4.7/5 rating | 10,000+ happy students | Great tutors 24/7